The commercial real estate crisis is poised to reshape the landscape of the real estate market in the coming years, particularly as high office vacancy rates persist. As businesses continue adjusting to post-pandemic work models, the demand for downtown office spaces has plummeted, leading to a significant decline in occupancy rates across major cities. Coupled with rising interest rates, this downturn raises concerns about a ripple effect within the banking system, potentially jeopardizing financial stability. With approximately 20% of the $4.7 trillion in commercial mortgage debt maturing this year, analysts are closely monitoring the economic impact that widespread delinquencies could have on our financial institutions. The stakes are high, and the path forward remains uncertain amid fears of widespread bank losses and failures.

The looming turmoil within the commercial property sector, often referred to as the commercial real estate downturn, threatens to shake the foundations of financial markets. With vacancy rates for office buildings reaching alarming heights, the reallocation of commercial spaces has become a pressing issue. This predicament is exacerbated by high interest rates, which have prompted some investors to reconsider their portfolios. The strain on the banking sector emphasizes the need for vigilant oversight as potential losses in commercial properties could reverberate through the broader economy. As experts weigh the implications of these developments, alternative strategies may be necessary to mitigate risks and ensure economic resilience.

High Office Vacancy Rates: A Looming Threat to the Economy

As office buildings stand underutilized, high vacancy rates are becoming a concerning trend across major U.S. cities. With figures ranging between 12 to 23 percent, the drop in demand for commercial office space since the pandemic is alarming. This shift is exacerbated by changing work patterns, with many companies adopting remote or hybrid models. The implications for the real estate market are severe; lower occupancy rates lead to depreciated property values, ultimately straining the economic framework. If landlords can’t maintain or attract tenants, this could ignite a ripple effect impacting everything from municipal tax revenues to local employment levels.

The longer these high vacancy rates persist, the more likely it is that smaller and regional banks, heavily invested in commercial real estate, will face unprecedented pressure. Financial experts fear that prolonged low demand could ultimately lead to a series of defaults on loans that were secured when occupancy rates were much more favorable. This might not only impair banking institutions but could also pose a risk to individuals and families reliant on regional banks for mortgages and personal loans.

The Commercial Real Estate Crisis: Causes and Consequences

The impending commercial real estate crisis can largely be attributed to a perfect storm of high inflation, rising interest rates, and poor market performance through the pandemic. Investors, having enjoyed a prolonged period of low borrowing costs, over-leveraged themselves in anticipation that these conditions would persist. When interest rates began their upward climb, many found their projects financially unfeasible, discovering that they were unable to refinance their debts as they matured. This reveals fundamental weaknesses in the banking system, highlighting how interconnected the fates of commercial real estate and financial institutions have become.

The economic impact of this crisis is not strictly confined to investors or banks; it extends to everyday consumers. If regional banks face significant losses on their commercial property loans, they could tighten lending standards impacting consumer credit availability. With consumers feeling the effects of a tightening banking system, this might lead to reduced spending, subsequently stifling economic growth. The potential risk here is not just isolated financial failure; it poses a broader threat to the economic stability of communities that depend upon healthy financial institutions.

Impact of Rising Interest Rates on Commercial Real Estate

The increase in interest rates has far-reaching implications for the commercial real estate sector. Initially, lower interest rates fueled high levels of borrowing and investment. However, as speculators and investors miscalculated their occupancy projections, the sharp rise in rates has turned these once-optimistic outlooks into substantial liabilities. Current assessments indicate that many property owners are grappling with the reality that their financial structures are being dismantled by the weight of increased repayments on loans. This adjustment period could be devastating for some, leading to foreclosures and an overall decline in property values.

Moreover, as interest rates remain elevated, potential buyers of distressed properties may opt to sit on the sidelines, further reducing demand. Consequently, markets may experience an oversupply of properties with few willing or able to invest. This stagnation won’t just hurt investors but could also impact local economies reliant on real estate transactions and developments for economic activity. Cities that experience a downturn in commercial real estate could witness cascading effects on job growth, infrastructure development, and overall economic dynamism.

Banking System Vulnerabilities Amid Potential Defaults

The commercial real estate sector’s downturn poses significant risks to the banking system, especially for smaller regional banks heavily invested in commercial loans. Assumptions that rising occupancy rates would translate into continued cash flows have led to cautionary warnings about a wave of upcoming delinquencies. As loans mature and investors scramble to refinance under deteriorating conditions, many banks may not sufficiently withstand the shocks resulting from these defaults. This could force institutions to absorb losses that were unimaginable just a few years ago.

The broader consequences of these stressors may lead to forced consolidations among weaker banks, igniting fears of a protracted financial crisis. While large banks might have regulatory safeguards in place, smaller banks that fail may not receive the same level of support, raising questions about systemic stability. In an environment where confidence is critical, the very existence of regional banks becomes precarious, posing a threat not only to the banking system but also to the economic security of communities dependent on those banks for stability.

Consumer Responses to the Commercial Real Estate Crisis

As the commercial real estate crisis unfolds, consumers may soon feel the implications on a personal level. If regional banks tighten lending standards in response to their potential losses in commercial real estate, individuals may find mortgages harder to secure, impacting home buying and consumer spending across various sectors. The concern extends beyond loans; diminished credit access can lead to a ripple effect that impacts everyday transactions, from car purchases to home renovations, as financial institutions become increasingly cautious.

Moreover, the downturn in commercial real estate could inadvertently lead to job losses, particularly in sectors tied to real estate development and management. Occupancy rates are sustained by consumer habits and business performance, and as this cycle turns, it may further drive uncertainty. As such, the economic environment will be complex, where some consumers benefit from a booming stock market while others face challenges stemming from increasing rates and reduced credit availability.

Adapting to Long-term Changes in the Real Estate Market

Given the long-term shifts in how we work and live — accelerated by the pandemic — the commercial real estate market will need to adapt to newfound realities. Many investors are beginning to shift focus toward properties that offer additional amenities and flexible workspaces as businesses explore how to draw staff back into offices amid higher occupancy rates. The onus now falls on developers to recalibrate their strategies to ensure they meet evolving consumer preferences while anticipating potential fluctuations in the economic landscape, including interest rates.

This means that some commercial spaces may need to be reimagined, leading to innovative architectural solutions that comply not just with zoning laws but also consumer needs for dwellings versus traditional office spaces. Successful adaptation could result in rejuvenated urban sectors that embrace dual-use or flexible spaces, driving a new economic model that aligns with contemporary lifestyle trends. As financial institutions reassess their risk profiles in the wake of this crisis, they may prioritize funding projects that demonstrate sustainable, adaptive reuse.

The Future Outlook of Commercial Real Estate

Looking ahead, the commercial real estate sector faces an uncertain landscape as banks, investors, and consumers navigate this pivotal transition. Predictions suggest that if long-term interest rates stabilize or decrease, some investors may regain footing allowing them to refinance outstanding debts before they reach a deadline. However, a future characterized by consistent changes in working patterns may continue to pressure office occupancy rates, creating a challenging environment for recovery.

Many stakeholders must remain vigilant as mechanisms for assessing risk evolve. Adaptability will become critical not only for investors but also for banking institutions that must remain resilient amid potential defaults on commercial loans. Whether through effective loan management practices or diversifying portfolios to mitigate risks, the real estate market, in conjunction with the banking system, will need to forge new pathways that not only weather the storm but also pave the way for future success.

Lessons from the Last Financial Crisis and Commercial Real Estate

Reflecting on the lessons from the 2008 financial crisis, stakeholders within the commercial real estate sector and banking institutions must prioritize prudence in an environment rife with speculation and borrowing. The mistakes of the past cannot be repeated; over-leveraging based on overly optimistic assumptions led to widespread financial disruptions, which have left a lasting impact on trust and systemic stability. Moving forward, risk assessment and management need to lead current practices highlighted by the necessity of sustainable investment preferences that guard against future shocks.

Furthermore, regulatory frameworks need explicit attention to ensure that banks remain robust against vulnerabilities associated with commercial real estate. This means more rigorous stress testing and capital requirements for lenders actively involved in commodity markets linked to property financing. Ultimately, the lessons learned during the last financial crisis should inform a proactive approach toward safeguarding the interconnectedness that defines the real estate market and banking system.

Cautious Optimism Amid the Commercial Real Estate Crisis

Despite the challenges posed by high vacancy rates and looming debt maturities, there exists a cautious optimism within segments of the market. Some investors remain hopeful that long-term interest rates might eventually drop, offering light at the end of the tunnel for struggling borrowers. The ongoing adaptation to new hybrid work arrangements could stimulate demand for redeveloped properties, turning previously unappealing spaces into vibrant business hubs once again.

Additionally, the emergence of innovative solutions aimed at repurposing underutilized office spaces into residential units may unlock hidden potential within urban landscapes. As cities pivot to meet the evolving demands of convenience and accessibility, the commercial real estate sector has the capacity to redefine itself into a more resilient and sustainable version of what it once was. Collectively, stakeholders must remain adaptable, maintaining a positive outlook amid the shifts in the real estate landscape.

Frequently Asked Questions

How will the commercial real estate crisis affect office-vacancy rates in major cities?

The commercial real estate crisis is expected to keep office-vacancy rates high in major cities. Currently, vacancy rates range from 12% to 23%, primarily due to decreased demand following the pandemic. As businesses continue to adjust to remote and hybrid work models, it’s likely that these occupancy rates will remain depressed, placing further pressure on property values and the overall economy.

What role do interest rates play in the commercial real estate crisis?

Interest rates significantly impact the commercial real estate crisis as rising rates have increased borrowing costs for investors. Many firms over-leveraged themselves when rates were low, which now poses risks as loans come due. With the Federal Reserve’s hesitation to lower rates, the financial strain on commercial real estate could exacerbate defaults and challenge the banking system.

How might the banking system be affected by the commercial real estate crisis?

The commercial real estate crisis could lead to increased delinquencies on loans, particularly affecting small and medium-sized banks that hold substantial commercial real estate debt. If these banks face significant losses, it may trigger tighter lending practices and lower consumption in the affected regions, impacting the broader economy.

What are the potential economic impacts of a commercial real estate crisis?

A commercial real estate crisis could lead to significant financial losses for banks, pension funds, and investors, which may ripple through the economy. Regions with higher exposure to affected banks might experience lower consumption and tighter credit. While the broader economy remains stable for now, a severe downturn could amplify these effects.

Can the commercial real estate crisis be mitigated, and if so, how?

Mitigating the commercial real estate crisis may require a reduction in long-term interest rates, enabling refinancing options for distressed properties. However, experts see this as unlikely outside of a significant recession. Likely, the market will see additional bankruptcies as firms adjust to the new economic realities, which is typical in the real estate sector.

What lessons can be learned from the commercial real estate crisis regarding investment strategies?

The commercial real estate crisis highlights the importance of caution in investment strategies, particularly in volatile markets. Investors must avoid over-leveraging and consider potential changes in economic conditions, such as rising interest rates and shifts in occupancy rates, to safeguard their portfolios against future downturns.

How can investors navigate the current challenges posed by the commercial real estate crisis?

Investors can navigate the challenges of the commercial real estate crisis by diversifying their portfolios, carefully assessing property values, and considering the potential for long-term vacancies. Staying informed about market trends and maintaining a conservative approach to borrowing will be essential in this uncertain environment.

| Key Points |

|---|

| High vacancy rates in office buildings range from 12% to 23%, damaging property values. |

| $4.7 trillion in commercial mortgage debt is due this year, risking bank stability and economy. |

| Many firms invested in commercial real estate may face significant losses but a total financial crisis is unlikely. |

| High-interest rates and pandemic-related demand drops have over-leveraged real estate investments. |

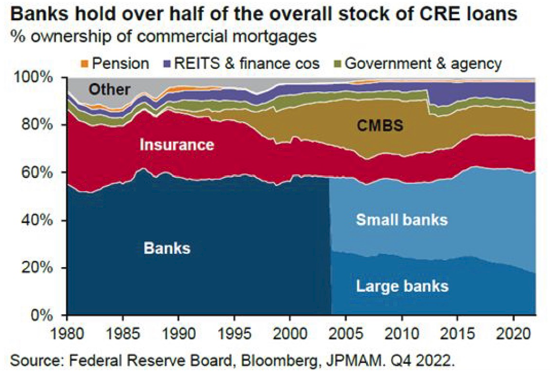

| While regional banks are vulnerable, larger banks may handle losses better due to diversification. |

| Some economists suggest long-term interest rate reductions could mitigate impacts on commercial real estate. |

| Bank failures could affect lending and consumption but are less likely to lead to a broader economic downturn. |

Summary

The commercial real estate crisis poses significant challenges as high vacancy rates and looming debt maturities threaten economic stability. Market experts assert that while many investors could experience substantial losses, a widespread financial meltdown is not imminent. The banking sector remains relatively shielded, particularly large institutions with diversified portfolios, although regional banks face potential vulnerabilities. Monitoring further developments and understanding the intricate dynamics in the commercial real estate market will be crucial as we navigate these tumultuous waters.