Corporate tax analysis plays a crucial role in understanding the financial landscape following the enactment of the 2017 Tax Cuts and Jobs Act. This significant tax reform aimed to lower corporate tax rates from 35% to 21%, which has since sparked intense debate among lawmakers and economists. The economic impact of tax cuts and subsequent corporate behavior has been a focal point in ongoing discussions about fiscal policy, particularly as the expiration of key provisions looms in 2025. Research by esteemed Harvard economist Gabriel Chodorow-Reich sheds light on the real effects of these changes, highlighting both modest increases in wages and business investment. As the tax reform debate continues, comprehending the implications of corporate tax policies will be essential for shaping future economic strategies.

Analyzing corporate taxation is essential for deciphering the effects of recent fiscal policies implemented through the 2017 Tax Cuts and Jobs Act. This landmark legislation effectively altered corporate tax obligations, reducing them significantly, and introduced a myriad of provisions aimed at stimulating economic activity. With the expiration of many of these measures approaching, the repercussions on business investments and fiscal health are coming under scrutiny. Esteemed voices in the field, such as economist Gabriel Chodorow-Reich, are providing data-driven insights into the repercussions of these tax reforms, fostering a deeper understanding of their effectiveness. As a national debate emerges over potential adjustments in corporate tax rates, it becomes increasingly vital to evaluate the economic realities influenced by these legislative changes.

Understanding Corporate Tax Rates: The Crucial Impact of the TCJA

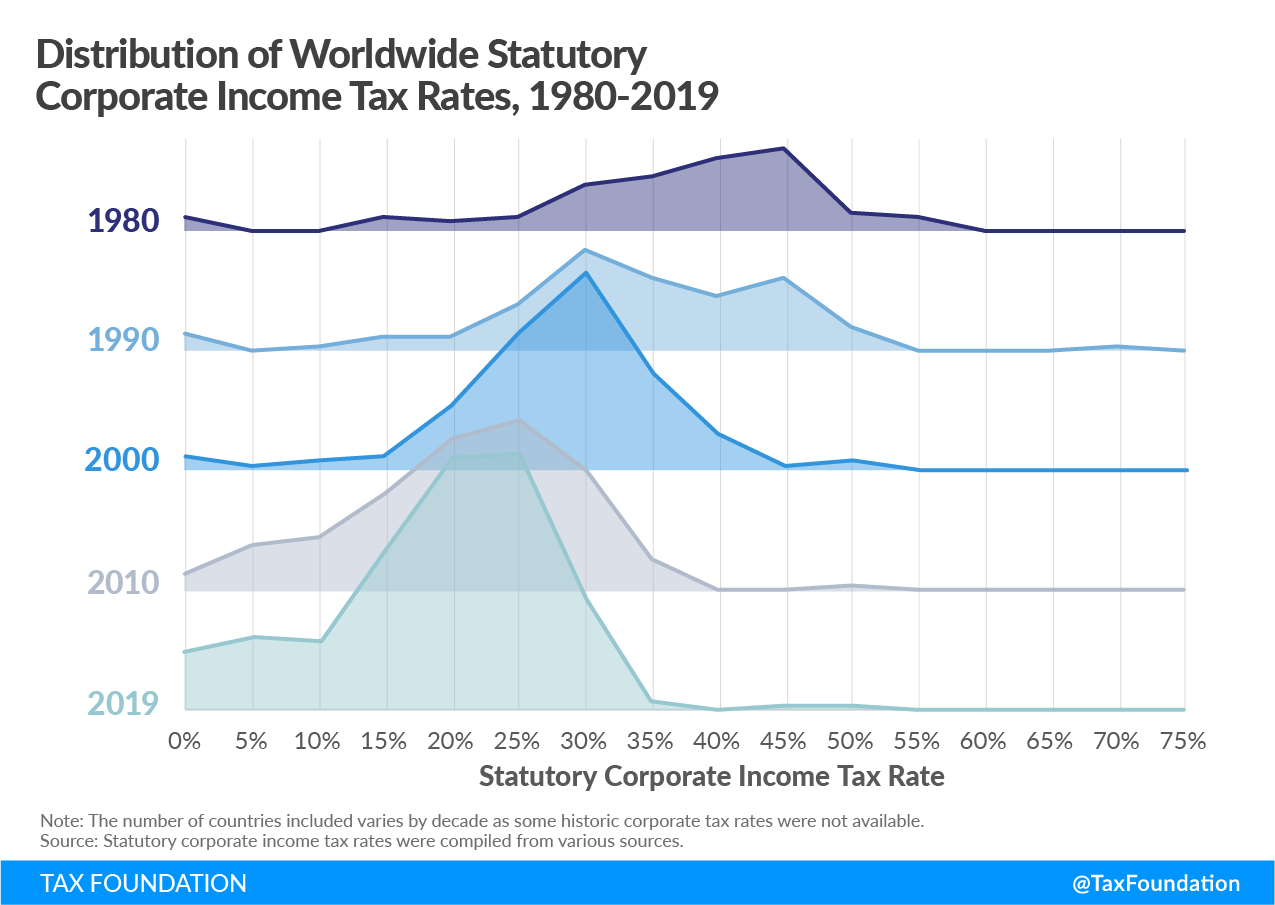

The Tax Cuts and Jobs Act (TCJA) significantly altered the landscape of corporate tax rates in the United States, reducing the statutory rate from 35% to 21%. This monumental shift has not only lowered the tax burden on corporations but has also raised questions about the long-term economic impacts. The corporate tax rate is a critical lever in economic policy, influencing business decisions related to investment, hiring, and expansion. By observing the reactions of firms post-TCJA, economists have gathered essential insights into the correlation between tax policy and corporate behavior, with implications for future legislative decisions.

Chodorow-Reich and his co-authors unveiled that while the corporate tax cuts did spur some increase in business investments, the broader economic implications—particularly regarding wage growth—remained modest. The analysis highlighted that while cuts can stimulate investment, they may not always translate into significant benefits for labor. Understanding these dynamics is crucial as lawmakers navigate the upcoming tax reform debate, especially with key provisions set to expire by 2025.

The Economic Impact of Tax Cuts: Myths and Realities

The economic impact of the TCJA is a topic of intense debate, particularly regarding the effectiveness of its corporate tax cuts. Proponents of the tax cuts argued that lowering corporate tax rates would lead to greater investment, job creation, and ultimately, wage increases for workers. However, empirical findings from Chodorow-Reich’s analysis suggest that the anticipated wage increases have been modest at best, countering assertions that tax cuts directly correlate with significant economic growth. Instead, the crucial lesson drawn from this research points to a more nuanced view of how corporate behavior is influenced by tax policy.

Chodorow-Reich emphasized that economic policy should not solely rely on the assumption that lowering taxes will automatically stimulate investment and wages. The reality is more complex; tax cuts might initially appear to promote business expansion, but the long-term effects often reveal a different picture. His research advocates for a balanced approach where policymakers consider the interplay of tax rates and targeted incentives, such as expensing provisions, to effectively drive economic growth without sacrificing necessary tax revenue.

The Future of Corporate Tax Analysis: A Call for Smarter Solutions

As Congress prepares for a tax battle in 2025, Gabriel Chodorow-Reich’s findings serve as a call to action for a re-evaluation of corporate tax policy. His work urges lawmakers to adopt a more analytical approach to corporate taxation, shedding light on the importance of evidence-based solutions rather than relying on partisan ideologies. The previous conclusions drawn from the TCJA about revenue losses and minimal wage growth compel legislators to consider alternative tax structures that could enhance government revenue without crippling economic incentives for businesses.

One potential path forward could involve raising corporate tax rates while simultaneously reinstating crucial expensing provisions that encourage capital investment. This dual approach could provide a more fertile ground for economic growth, benefiting both corporations and employees. Policymakers must remain cognizant of the broader economic context and the lessons learned from past reforms to create a framework that is both economically sustainable and equitable.

Evaluating the 2017 Tax Cuts: A Closer Look at Their Fiscal Outcomes

The fiscal outcomes of the 2017 Tax Cuts and Jobs Act revealed shocking consequences for corporate tax revenue, which dropped by 40% immediately following the law’s enactment. This significant decrease raised alarms about long-term budget deficits, with challenges looming high as Congress looked to restore critical tax benefits. The complexities surrounding the TCJA highlight the need for an in-depth evaluation of tax reform measures, not only in terms of their immediate impacts but also in their sustainability and effectiveness.

As the expiration of key provisions approaches, economists like Chodorow-Reich are calling for a systematic reevaluation of the TCJA. With insights gained from comprehensive empirical studies, the emphasis is shifting towards understanding how these tax cuts have affected investment patterns and government revenue streams. By exploring these economic relationships, policymakers can ground future legislative debates in sound analysis instead of partisan divisiveness.

Corporate Tax Revenue Trends Post-TCJA: Understanding the Ups and Downs

Post-TCJA, corporate tax revenue trends revealed an unexpected recovery, soaring beyond initial forecasts as corporate profits rose sharply during the pandemic. This trend invites scrutiny into the factors that contributed to this resurgence, including changes in corporate behavior and market adaptations, such as supply chain adjustments. Such a phenomenon challenges preconceived notions about corporate tax cuts leading to diminished government coffers, prompting the need for further exploration into the dynamics of tax policy and corporate earnings.

Chodorow-Reich’s analysis indicates that monitoring revenue streams post-TCJA must take into account varying market conditions, indicating a correlation between corporate tax policies and societal economic shifts. As observers analyze these developments, the results could inform future tax policy, ensuring that lawmakers approach reforms with clarity about their potential revenue implications.

The Political Debate Over Corporate Tax Reform: Challenges Ahead

As the political landscape heats up regarding corporate tax reform, the positions of prominent leaders crystallize the contentious nature of this discussion. With Vice President Kamala Harris advocating for increased corporate tax rates to support broader social spending initiatives, and former President Donald Trump arguing for further reductions to stimulate economic growth, the battlefield is set for renewed debate. This political dichotomy underscores underlying ideological divides on taxation and economic policy, compounding the challenges policymakers face as they seek to navigate these waters.

Recent studies have become vital in the ongoing tax reform debate, providing a platform for evidence-based policy decisions amid rising partisan rhetoric. Chodorow-Reich’s findings help to illuminate the effects of tax policies on corporations, thereby providing insights that could forge pathways towards productive negotiations among lawmakers. Ultimately, a collaborative effort is required to address fiscal challenges while balancing economic growth, ensuring that future reforms reflect both the realities of the corporate tax landscape and the expectations of the electorate.

The Role of Expiring Tax Provisions: What Lies Ahead?

With the expiration of several key tax provisions on the horizon, the implications for corporate taxation and economic performance are becoming increasingly dire. Chodorow-Reich and his colleagues have indicated that some of the most effective components of the TCJA included provisions allowing immediate write-offs of capital investment costs. The potential losses from allowing these provisions to lapse emphasize the importance of timely legislative action to avoid disrupting business investments that are critical to economic growth.

The urgency to address these expiring provisions is amplified by the upcoming political cycle. As corporate tax cuts are strategically employed in election rhetoric, it will be critical for lawmakers to consider the long-term impact of these decisions on both fiscal revenue and economic health. Investing in smart policy choices, rather than strictly following short-term political agendas, could yield significant benefits for both corporations and the workforce.

Capital Investment and Wages: Analyzing the Relationship

The connection between capital investment induced by corporate tax policy and its effect on wage growth is a focal point of economic discussions today. Many believed that the TCJA would lead to significant wage increases, yet analyses have shown that the relationship is more complex. Chodorow-Reich’s research suggests that while capital investments indeed increased, the resulting wages did not meet earlier projections. This disparity ignites ongoing inquiry into the mechanisms by which tax policy influences not only corporate behaviors but also outcomes for employees.

Understanding the true dynamics between investment and wages is crucial as companies are expected to hire more workers in response to increased capital. In situations where businesses acquire more resources, the expectation is that competition for labor drives wages upward. Policymakers must reflect on these relationships to create tax frameworks that foster genuine growth for the workforce while meeting corporate needs.

Lessons from the TCJA: Insights for Future Tax Reforms

The insights garnered from the TCJA’s implementation present invaluable lessons for future tax reforms. One key takeaway is the necessity for policymakers to base their decisions on empirical evidence rather than ideological beliefs. Chodorow-Reich’s analysis sheds light on the need for a balanced approach to corporate taxation that optimizes investment without undermining essential revenue streams. Thus, future reforms must aim at embracing flexibility and adaptability in tax structures to respond to evolving economic realities.

Moreover, as discussions around corporate tax rates continue, the importance of understanding the broader implications of such decisions becomes clear. Striking a balance between incentivizing business growth and ensuring sufficient government funding requires insightful policymaking informed by comprehensive data. The TCJA experience serves as a pivotal case for examining how tax legislation can influence economic dynamics and offers a framework for crafting effective future policies.

Frequently Asked Questions

What is the impact of the 2017 Tax Cuts and Jobs Act on corporate tax analysis?

The 2017 Tax Cuts and Jobs Act (TCJA) significantly altered corporate tax analysis by reducing the statutory corporate tax rate from 35% to 21%. This change spurred debate regarding its economic impact, particularly on wages and business investments. Research, including studies by economist Gabriel Chodorow-Reich, has shown that while capital investments rose by about 11% post-TCJA, the expected wage increases fell short of projections, highlighting the complexity of tax reform consequences.

How did corporate tax rates change under the 2017 Tax Cuts and Jobs Act?

Under the 2017 Tax Cuts and Jobs Act, corporate tax rates were permanently lowered from 35% to 21%. This reduction aimed to make U.S. businesses more competitive globally but raised concerns about a potential drop in federal revenue, projected to decrease by $100 billion to $150 billion annually over the next decade.

What were the economic effects of tax cuts on corporate profits post-TCJA?

Post-TCJA, corporate profits surged beyond expectations, leading to a significant increase in federal corporate tax revenue after an initial drop of 40% following the law’s enactment. The rebound in revenue is linked to higher-than-forecasted business profits, with factors such as supply chain changes and the abandonment of low corporate rates in Ireland being potential contributors to this trend.

What does Gabriel Chodorow-Reich’s analysis reveal about corporate tax policy?

Gabriel Chodorow-Reich’s analysis emphasizes the necessity of a nuanced understanding of corporate tax policy impacts. His research indicates that while the TCJA resulted in modest increases in corporate investments, it failed to provide the significant wage growth initially projected. This points to the need for a comprehensive corporate tax analysis that factors in both immediate and longer-term economic effects.

What provisions of the TCJA are expiring and what implications might this have for corporate tax analysis?

Several key provisions of the TCJA, particularly those enhancing expensing for new capital investments, are set to expire at the end of 2025. This expiration could lead to decreased corporate investments and revenues, necessitating a reevaluation of corporate tax analysis that considers the effectiveness of temporary versus permanent tax cuts on business behavior.

How does the corporate tax reform debate influence economic policy?

The corporate tax reform debate, fueled by contrasting views on raising or cutting tax rates, directly influences economic policy. Figures like Kamala Harris advocate for higher corporate rates to fund social initiatives, while others argue for lower rates to promote growth. This ongoing discussion shapes legislative approaches to tax policy, especially as key TCJA provisions approach expiration.

What lessons can be learned from the 2017 Tax Cuts and Jobs Act for future corporate tax legislation?

Lessons from the 2017 Tax Cuts and Jobs Act underline the importance of empirical analysis in assessing tax reforms. Chodorow-Reich’s findings suggest that temporary expensing measures may drive more effective investment than static rate cuts. Future corporate tax legislation should consider the nuanced relationship between tax rates and investment behavior to devise more effective economic policies.

Why is corporate tax analysis important for understanding the economic impact of tax cuts?

Corporate tax analysis is critical for understanding the economic impact of tax cuts because it evaluates how changes in tax policy affect business decisions regarding investment, wages, and overall economic growth. Analyzing these effects helps policymakers predict the long-term fiscal and economic consequences of tax law changes, ensuring informed legislative decisions.

| Key Points |

|---|

| Corporate tax rates are under debate as Congress prepares for 2025 tax legislation, with key parts of the 2017 tax law expiring soon. |

| The 2017 Tax Cuts and Jobs Act (TCJA) reduced the corporate tax rate from 35% to 21%, significantly impacting federal tax revenue. |

| The TCJA, while intended to stimulate growth through lower rates, has shown only modest increases in wages and business investments. |

| Chodorow-Reich’s analysis suggests that expired provisions, which allowed immediate expensing, were more effective in driving investment than rate cuts. |

| Debate continues over how corporate taxation influences both investment and wage growth, with substantial variance in predictions and outcomes. |

| Corporate tax revenue decreased by 40% immediately post-TCJA but rebounded due to higher-than-expected profits during the pandemic. |

Summary

Corporate tax analysis reveals that the ongoing discussions about corporate tax rates are crucial as we approach significant legislative changes in 2025. The mixed results from the 2017 Tax Cuts and Jobs Act underline the complexity of tax policy, urging stakeholders to consider the balance between stimulating economic growth and maintaining sufficient government revenue. As various provisions expire, strategic reevaluations could pave the way for more effective fiscal policy that meets the needs of a globalized economy.